In today’s fast-paced digital economy, payment services like Perpay have become increasingly popular among consumers looking for flexible and convenient ways to manage their purchases. As more people turn to buy now, pay later (BNPL) options, it’s essential to understand whether these services are legitimate and how they compare to traditional financial tools. This article will explore the legitimacy of Perpay, its features, benefits, and potential drawbacks, providing a clear picture of what users can expect.

Understanding Perpay: What Is It?

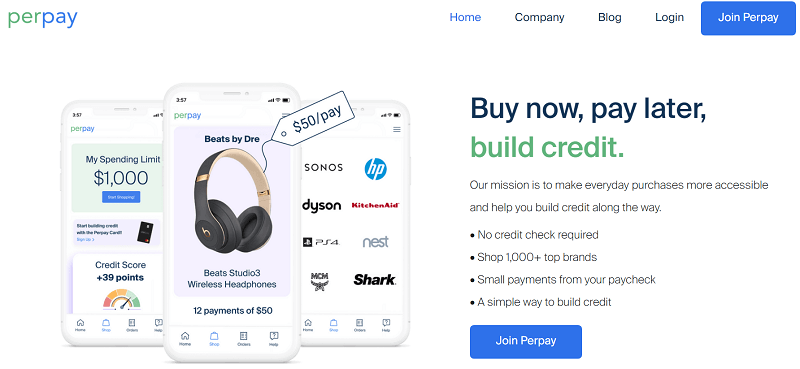

Perpay is a buy now, pay later (BNPL) service that allows users to split their purchases into manageable installments, which are automatically deducted from their paycheck. Unlike other BNPL platforms, Perpay operates exclusively within its own marketplace, meaning users can only shop with retailers that partner with Perpay. The service does not charge interest or late fees, making it an attractive option for those who want to avoid high-interest debt.

To use Perpay, users must first create an account and provide proof of full-time employment, as well as meet certain eligibility requirements. Once approved, users receive a spending limit based on their income and can then make purchases through the Perpay marketplace. Payments are structured to be deducted from each paycheck until the total amount is paid off.

How Does Perpay Work?

The process of using Perpay is straightforward:

- Sign Up: Users download the Perpay app or visit its website and create an account by providing personal information, including age, address, phone number, and proof of employment.

- Approval: Perpay reviews the application and approves users who meet its criteria, such as being a full-time W-2 employee with at least three months of continuous employment.

- Set Spending Limit: Based on the user’s income, Perpay sets a spending limit. This limit can be increased over time with consistent, on-time payments.

- Shop: Users can browse the Perpay marketplace, which includes major brands like Apple, PlayStation, and Dyson.

- Checkout: At checkout, users choose how many payments they want to make, with options up to six months.

- Payment Plan: The selected payment plan is automatically deducted from the user’s paycheck each time they receive their salary.

One unique feature of Perpay is that payments are only processed after the first payment is made. This means that users must wait until their next payday for the order to ship, ensuring that the payment is in place before the item is delivered.

Key Features and Benefits of Perpay

Perpay offers several features that set it apart from other BNPL services:

- No Interest or Late Fees: Perpay does not charge interest on purchases and also does not impose late fees, even if payments are missed.

- Customizable Repayment Plans: Users can choose how many payments they want to make, with the option to pay off the balance faster by increasing the direct deposit amount.

- Credit Building Option: For an additional monthly fee of $3, users can opt into Perpay+, which reports their payment history to the three major credit bureaus (Experian, Equifax, and TransUnion). This can help improve credit scores over time.

- Easy to Use: The Perpay app has received high ratings on both the Apple App Store and Google Play, with users praising its intuitive design and ease of navigation.

However, there are some limitations to consider. For instance, Perpay is only available to full-time W-2 employees, which excludes gig workers and self-employed individuals. Additionally, the service is limited to its own marketplace, which may not include all the retailers users typically shop at.

Perpay vs. Other BNPL Services

When compared to other BNPL providers like Affirm, Klarna, and Afterpay, Perpay stands out in a few key areas:

- Repayment Flexibility: While most BNPL services offer fixed repayment terms (e.g., four equal payments over six weeks), Perpay allows users to choose how many payments they want to make, up to six months.

- No Interest Charges: Like many BNPL services, Perpay does not charge interest, but it also avoids late fees, which is a significant advantage over competitors like Afterpay.

- Limited Retailer Access: Unlike other BNPL services that integrate directly with thousands of retailers, Perpay is confined to its own marketplace, which may restrict users’ choices.

Despite these differences, Perpay has earned a reputation for reliability and customer satisfaction. Its A+ rating from the Better Business Bureau (BBB) and positive reviews from users indicate that it is a legitimate service.

Is Perpay Trustworthy?

Perpay has been rated A+ by the Better Business Bureau, which evaluates companies based on their responsiveness to customer complaints, honesty in advertising, and transparency in business practices. While this rating suggests that Perpay is generally trustworthy, it’s important to note that no company is without its critics.

Some users have reported issues with the service, including:

- High Prices: Many users have noted that items on the Perpay marketplace are often priced higher than on other retailers, sometimes by as much as 75%.

- Slow Customer Service: Perpay does not list specific hours for customer service, and some users have found it difficult to get timely assistance.

- Shipping Delays: There have been reports of orders taking longer than expected to arrive, with some users waiting over 21 days for their items.

Despite these concerns, Perpay remains a viable option for those who meet its eligibility requirements and are willing to accept its limitations.

Perpay Pros and Cons

Pros

- No impact on your credit score when applying

- Flexible repayment plans up to six months

- No interest or late fees

- Credit building option available for an additional fee

- Easy-to-use mobile app

Cons

- Only available to full-time W-2 employees

- Limited to Perpay’s marketplace

- Higher prices on some items

- No direct integration with popular retailers like Amazon

- Limited customer service availability

Who Should Use Perpay?

Perpay is best suited for:

- Full-time W-2 employees who want to spread out their payments over time

- Individuals with poor or no credit who want to build their credit history through Perpay+

- Those looking for a no-interest, no-late-fee alternative to traditional credit cards

However, it may not be the best choice for:

- Gig workers or self-employed individuals

- Users who prefer to shop on other platforms like Amazon

- People who need immediate access to funds

Perpay Alternatives

For those who don’t qualify for Perpay, there are several alternatives worth considering:

- Affirm: Offers flexible repayment plans and integrates with a wide range of retailers.

- Klarna: Provides “pay later” options and works with major online stores.

- Afterpay: Allows users to split purchases into four installments, though it charges late fees.

- PayPal Credit: A credit line that can be used for online purchases and offers rewards.

Each of these services has its own set of pros and cons, so it’s important to evaluate them based on your specific needs and financial situation.

Final Verdict: Is Perpay Legit?

Yes, Perpay is a legitimate buy now, pay later service with a strong reputation and positive user reviews. It offers a flexible, no-interest way to manage purchases and provides an opportunity to build credit for an additional fee. However, it has some notable limitations, including its exclusive marketplace and eligibility requirements.

If you’re a full-time W-2 employee looking for a reliable and user-friendly BNPL option, Perpay could be a good fit. But if you’re a gig worker or prefer to shop on other platforms, you may want to explore alternatives.

Frequently Asked Questions

Q: Is Perpay safe?

A: Yes, Perpay uses SSL technology and 128-bit encryption to protect user data. It also has an A+ rating from the Better Business Bureau.

Q: Can I use Perpay to buy anything?

A: No, Perpay is limited to its own marketplace, which includes select retailers.

Q: Does Perpay report to credit bureaus?

A: Only if you sign up for Perpay+, which costs $3 per month.

Q: Can I pay off my balance early?

A: Yes, you can increase your direct deposit amount to pay off your balance faster.

Q: What happens if I miss a payment?

A: Perpay does not charge late fees, but missing payments can affect your credit score if you’re enrolled in Perpay+.

Conclusion

Perpay is a legitimate and innovative payment service that offers a unique approach to buying now and paying later. With its no-interest model, flexible repayment options, and credit-building feature, it can be a valuable tool for eligible users. However, its limitations—such as restricted retailer access and strict eligibility requirements—may make it unsuitable for everyone.

Before signing up, it’s important to weigh the pros and cons and determine whether Perpay aligns with your financial goals and shopping habits.

Stay updated with the latest news and insights on financial services and consumer trends.

More Stories

How to Claim Your Joy in League of Legends: A Step-by-Step Guide

What is WSET? A Comprehensive Guide to Wine Education

How Will VA Compensation Be Affected by a Government Shutdown?